Adjustable-rate mortgages (ARMs) are coming back stronger than ever amid high interest rates. Why are more people choosing ARMs over fixed-rate mortgages? Because, in the long run, an ARM may actually be more beneficial.

Homebuyers that choose a fixed-rate mortgage over an ARM typically do so because of the stability offered from the fixed-rate. That is a great option for many borrowers. However, with today’s high rates, borrowers are turning to adjustable-rate mortgages in the hope of getting a lower interest rate down the road.

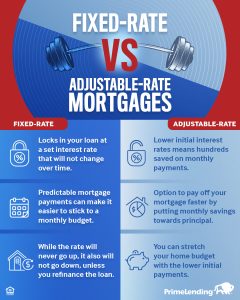

FIXED-RATE VS. ADJUSTABLE-RATE MORTGAGE: WHICH IS BETTER

Fixed-rate and adjustable-rate mortgages are the two most common mortgage options for borrowers. So, what is the difference between a fixed-rate and adjustable-rate mortgage? Is one better than the other? Let’s find out.

A fixed-rate mortgage locks in your loan at a set interest rate that will not change over the life of your loan. Since the rate won’t change over time, it makes it easier to know your monthly budget because your mortgage payment is predictable. While your rate will never go up, it will also never go down—unless you refinance at the right time, but that is a conversation for a different blog.

ARMs on the other hand are more variable than fixed-rate mortgages. An adjustable-rate mortgage has a set “introductory” interest rate that is typically lower than that of conventional loans. This rate stays the same for a certain amount of time, usually several years.

HOW AN ADJUSTABLE-RATE MORTGAGE WORKS

If you look at an ARM loan, you’ll see it shown as X/Y. But, if you aren’t familiar with how adjustable-rate mortgages work, those numbers may mean nothing to you. Luckily, I have an example ready to show you why they should mean something.

Say you apply for a 5/6 ARM. The 5 is the length of your introductory period. That means that for 5 years your interest rate won’t change. The 6 represents how often the rate can change for the life of your loan. So, after the initial 5 years, your rate will change every 6 months until you are done with that loan. The good news is the rate change only applies to the remaining years and balance of your mortgage.

Worried about run-away interest rates? Don’t be. ARM home loans have an adjustment cap and a lifetime cap which limit how much an interest rate can adjust in one period and over the loan term.

BENEFITS OF GETTING AN ADJUSTABLE-RATE MORTGAGE

Adjustable-rate mortgages offer flexibility that conventional loans do not. ARMs are great for homebuyers who are purchasing a starter home or plan to move before the rate changes. Other benefits include:

- A lower initial interest rate

- A lower starting monthly payment

- The opportunity to purchase a house with more square footage

- The possibility of paying less in return with favorable market conditions

Ready to flex the buying power an ARM can give you? Talk to a PrimeLending loan expert today to get started.